2025 is regarded as the inaugural year of a "mild growth cycle" for the global stainless steel industry. Amid the dual pressures of a sluggish global manufacturing recovery and rising trade protectionism, the center of gravity for industrial supply has accelerated its shift toward Asia. Southeast Asia, in particular, has emerged as the core source of global incremental growth. Concurrently, the advancement of carbon neutrality policies and significant regional disparities in energy costs are driving the global market toward a bifurcated "regionalized" landscape. Industry competition is evolving from simple scale expansion to deep structural optimization and green transformation.

I. 2025 Overseas Market Review: Southward Shift and Zero-Sum Dynamics

Regional Supply: Indonesia’s Dominance and India’s Rise

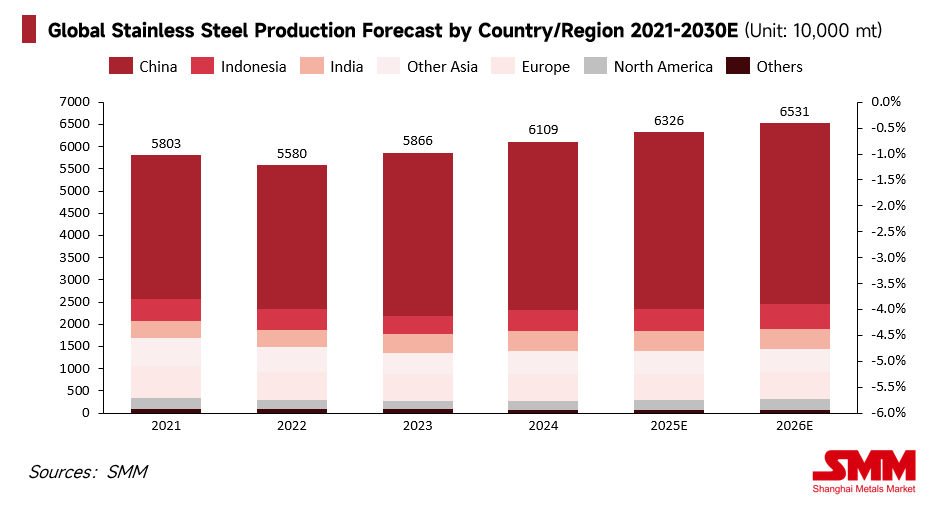

According to SMM data, in 2025, global crude stainless steel production remained high at approximately 63.26 million tons, with Asia’s share of production further climbing to around 86% of the global total. Leveraging highly competitive raw material costs and the advantages of integrated RKEF (Rotary Kiln Electric Furnace) processes, Indonesia maintained a rapid growth rate of approximately 6.2%. This not only solidified its position as the global source of low-cost stainless steel slabs and hot-rolled coils but also profoundly reshaped global trade flows.

Meanwhile, India emerged as another major growth pole. Driven by robust infrastructure investment and domestic manufacturing policies, India’s capacity expanded steadily. By establishing non-tariff barriers such as BIS certification, India successfully built a defensive system, effectively replacing imports with domestic supply and joining Indonesia as a dual engine for Asian growth.

The Western Dilemma: High Energy Costs and Capacity Marginalization

In contrast to the vibrant Asian market, the stainless steel industries in Europe and North America faced severe survival challenges in 2025. Squeezed by the "triple threat" of high energy costs, elevated labor expenses, and increasingly stringent environmental compliance requirements, high-cost capacity in the West accelerated toward marginalization. Many plants operated at low utilization rates or entered prolonged shutdowns. To protect fragile domestic supply chains, Western nations resorted to high trade barriers, including increased tariffs, anti-dumping investigations, and the early deployment of the Carbon Border Adjustment Mechanism (CBAM). While this defensive posture slowed the shrinkage of domestic markets, it also caused Western stainless steel prices to decouple from global benchmarks, resulting in significant premiums.

Macro Environment: The "Scissors Gap" between Rate Cuts and Weak Manufacturing

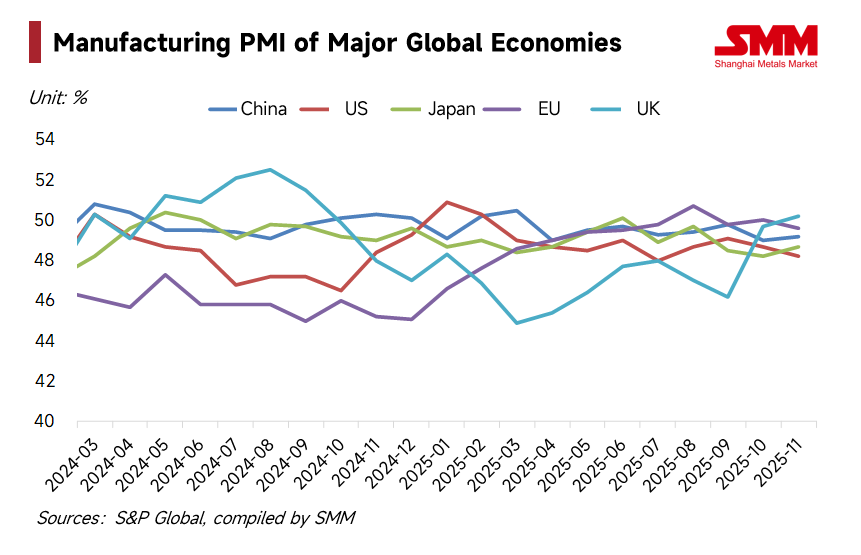

At the macro level, the Federal Reserve entered a rate-cutting cycle in 2025, providing a degree of bottom support for metal prices through improved global liquidity. However, this monetary easing failed to translate quickly into physical demand. Manufacturing PMIs in the U.S. and Europe fluctuated below the expansion-contraction threshold for much of the year. This "loose money, weak demand" pattern led to sluggish consumption growth in high-end manufacturing, appliances, and durable goods. Coupled with persistent supply-side easing, stainless steel prices encountered significant resistance during rallies, resulting in a market characterized by wide fluctuations and narrowing profit margins.

Raw Material Performance: Supply Volatility, Cost Pulses, and Strategic Scrap Use

The cost side of stainless steel showed extreme sensitivity and uncertainty in 2025, with raw material fluctuations directly defining the survival boundaries of enterprises. As the core supplier, Indonesia’s erratic RKAB (Work Plan and Budget) approval progress became a key variable. Quota shortages triggered rapid surges in ferronickel costs, creating "pulse-like" spikes. Meanwhile, global reliance on South African chrome ore remained high. Limited by local logistical bottlenecks and rising electricity costs, ferrochrome prices fluctuated at high levels, providing a firm floor for stainless steel prices.

Notably, the raw material structure in the European market underwent a qualitative change. Despite weak demand for finished products, the price of austenitic scrap (304 grade) remained exceptionally firm. This was driven by leading European mills aggressively increasing scrap ratios to replace primary raw materials and reduce their carbon footprint. In this context, scrap evolved from a simple cost-adjustment tool into a key strategic resource, with its pricing logic increasingly tied to carbon emission reduction values. This heavy reliance on specific regional supplies or low-carbon resources has prompted companies to accelerate the layout of diversified supply chains, making long-term agreements and raw material self-sufficiency core metrics of competitiveness.

Demand Analysis: Regional Polarization and Structural Transition

Global consumption in 2025 exhibited extreme regional divergence. Under the lingering effects of high inflation and energy costs, consumption of appliances and durables in the West remained depressed.

- Europe: The market fell into a stalemate. Facing uncertain macro demand, European distributors adopted extremely conservative inventory strategies, maintaining only "hand-to-mouth" procurement. This led to a sharp drop in shipments from major European mills, with order visibility hitting historic lows. While mills attempted to pass on costs via high "alloy surcharges," base prices remained suppressed by fierce competition from low-priced Asian imports, despite trade safeguards.

- North America: A profound supply chain restructuring is underway. Facing geopolitical uncertainties, North American buyers accelerated the regionalization of their supply chains in 2025. To mitigate transoceanic logistical risks (e.g., the Red Sea crisis) and potential tariff fluctuations, many shifted their procurement focus from Asia to Mexico or Canada. This "near-shoring" trend prompted mills to adjust their capacity layouts and supply priorities within the Americas.

- Green Premium Reality: Market feedback in 2025 revealed that a "green premium" is not yet universal. The willingness to pay extra is currently concentrated in niche sectors where end-users have clear Scope 3 reduction targets (e.g., EU public procurement, multinational consumer brands). In broader construction and general industrial sectors, price remains the sole deciding factor.

As the EU further tightens imports through CBAM and safeguards, products from China, Taiwan (China), and Indonesia originally destined for Europe may flow back into Asia, potentially turning the ASEAN market into a "dumping ground" for low-priced goods.

II. 2026 Market Outlook: Rule Changes and Logic Reconstruction

Green Trade: The Substantive Impact of the CBAM Charging Period

Looking ahead to 2026, the most critical turning point in global trade will be the official commencement of the CBAM charging period. This means Asian suppliers relying on coal power and traditional RKEF processes will face significant carbon tax costs when exporting to Europe. This policy will force factories in Indonesia and elsewhere to accelerate the transition from "black" to "green" energy or seek alternative markets with lower carbon barriers, such as Eastern Europe or parts of Southeast Asia. 2026 will witness the substantive transformation of carbon emission rights from an "environmental concept" into a "production cost."

Supply-Demand Pattern: Further Market Fragmentation

Global crude stainless steel production is expected to maintain a modest compound growth rate of about 2.5% in 2026. However, this growth will be geographically uneven. The global market will further split into two parallel worlds:

- High-Price Closed Zones (West): Characterized by high tariffs and carbon taxes, regional prices will remain high, but total demand growth will be stagnant due to the slow return of manufacturing.

- Intense Competition Zones (SEA, Middle East, Africa): Capacity from Indonesia, China, and India will engage in fierce cost-based competition, significantly increasing market volatility.

Pricing Logic: External Drivers for Steady Recovery

SMM believes that global stainless steel prices will enter a steady and moderate recovery track in 2026. This recovery will not be driven by explosive terminal demand, but rather by substantive improvements in the global macro environment and the endogenous repair momentum of the industrial chain after a period of deep profit inversion.

As inflationary pressures ease and financing costs in major economies decline, the release of global liquidity will slowly lift the pricing center for stainless steel. Furthermore, after the extreme cycle of 2025 where margins were squeezed to their limits, the production side will show a strong desire for price recovery. This repair logic is not just a result of rigid cost support, but a natural outcome of the industry attempting to reverse the unsustainable state of long-term cost-price divergence through production cuts and price-holding strategies.

Additionally, pricing logic will return further to industrial fundamentals. The Indonesian government is expected to continue tightening export quota management for mineral resources and guiding the industry toward high-value-added downstream processing. This may drive structural changes in global nickel flows. With the implementation of "anti-involution" (anti-cutthroat competition) policies and the natural exit of overcapacity, the global supply-demand balance is expected to see marginal improvement. The core focus of competition will shift systematically toward green/low-carbon levels, cost resilience, and the ability to capture structural growth opportunities.

Conclusion: Finding Structural Opportunities Amid Uncertainty

The 2025 review reveals an industry undergoing profound transition, while the 2026 outlook points to a more complex future governed by "rule-based" competition. In the context of global supply chain restructuring, stainless steel enterprises must find a balance between enhancing low-carbon competitive advantages and optimizing global supply chain layouts. The future winners will no longer be those who rely solely on scale, but those who can flexibly allocate resources in a fragmented market, navigate trade barriers, and lead the green transition.

Written by: Bruce Chew

![[SMM Stainless Steel Flash] April 2, 2026: Stainless Steel Market Highlights](https://imgqn.smm.cn/usercenter/biBGl20251217171733.jpg)

![[SMM Analysis] Nickel Salt Prices Edge Down Amid Weak Downstream Demand and Rising Raw Material Costs](https://imgqn.smm.cn/usercenter/yaAtG20251217171733.jpg)